Impulse spending is one of the biggest silent threats to financial stability. It doesn’t always look dramatic. It’s not necessarily a luxury car purchase or an extravagant vacation. More often, it’s small, frequent, emotionally driven purchases—a flash sale you didn’t plan for, late-night online shopping, an extra item tossed into your cart “just because,” or daily takeout that slowly adds up.

In today’s digital world, resisting impulse spending is harder than ever. Online stores are open 24/7. Ads are personalized. One-click checkout makes purchases effortless. Social media platforms like Instagram and TikTok constantly showcase trending products, limited-time deals, and influencer recommendations that trigger the fear of missing out (FOMO). Meanwhile, e-commerce giants like Amazon make it incredibly easy to buy something within seconds.

The problem isn’t just the money spent—it’s the habit. Impulse spending often stems from emotions: stress, boredom, celebration, sadness, or even procrastination. Over time, it can sabotage savings goals, delay debt repayment, and create financial anxiety.

The good news? Impulse spending is a behavior—and behaviors can be changed. You don’t need extreme budgeting tactics or complete deprivation. What you need is awareness, practical strategies, and systems that make smart spending easier than emotional spending.

If you’re ready to take control of your finances and stop feeling guilty after unnecessary purchases, this guide will show you exactly how to stop impulse spending for good.

1. Identify Your Spending Triggers

Before you can stop impulse spending, you need to understand why it happens.

Ask yourself:

- Do I shop when I’m stressed?

- Do I buy things when I’m bored?

- Am I influenced by social media trends?

- Do I feel pressure during sales events?

Track your purchases for 30 days and note the emotion behind each unplanned expense. Patterns will quickly emerge.

2. Implement the 24–48 Hour Rule

One of the simplest and most powerful strategies is delaying the purchase.

When you see something you want:

- Wait 24–48 hours.

- Add it to a wish list instead of your cart.

- Revisit it later.

Most impulse urges fade with time. If you still want the item after waiting, you can evaluate it rationally.

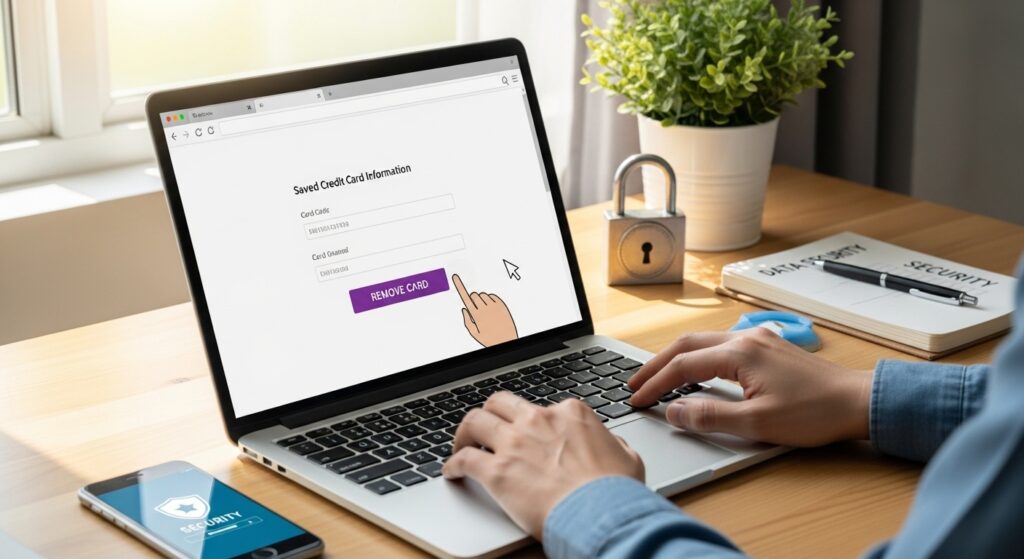

3. Remove One-Click Convenience

Convenience fuels impulsivity.

To create friction:

- Remove saved credit cards from websites.

- Log out of shopping apps.

- Disable one-click purchasing.

- Unsubscribe from promotional emails.

Making purchases slightly less convenient gives your brain time to think before acting.

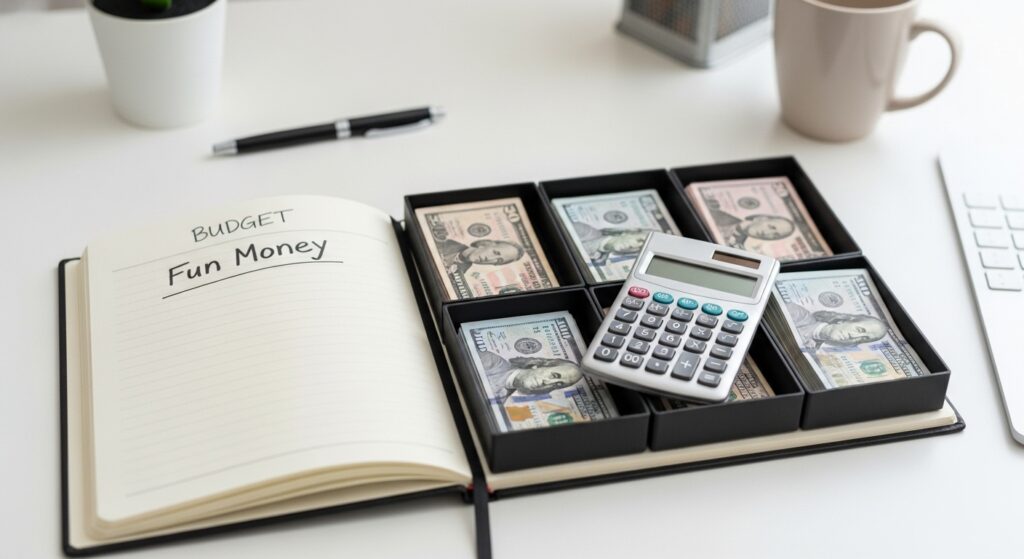

4. Set a Monthly “Fun Money” Limit

Completely restricting yourself can backfire. Instead, allocate a reasonable monthly amount for discretionary spending.

This allows you to:

- Enjoy guilt-free purchases.

- Stay within financial boundaries.

- Avoid binge spending later.

When your fun money is gone, pause until the next month.

5. Avoid Emotional Shopping Environments

If certain environments trigger spending, reduce exposure.

For example:

- Avoid browsing shopping apps for entertainment.

- Unfollow influencers who promote constant product buying.

- Stay out of stores when you’re stressed.

Replace shopping with healthier alternatives:

- Exercise

- Reading

- Journaling

- Calling a friend

6. Create Clear Financial Goals

It’s easier to resist impulse purchases when you have something bigger to work toward.

Examples:

- Emergency fund

- Debt freedom

- Vacation savings

- Home down payment

- Investment portfolio

Write your goal somewhere visible. When tempted to buy, ask:

“Is this more important than my long-term goal?”

7. Use Cash for Discretionary Spending

Using physical cash can reduce overspending. Studies show people spend less when paying with cash compared to cards.

Withdraw your monthly discretionary allowance and place it in an envelope. When it’s empty, you’re done spending for the month.

8. Track Progress and Celebrate Wins

Breaking impulse spending habits takes time.

Track:

- Money saved monthly

- Reduced unplanned purchases

- Progress toward goals

Celebrate milestones in healthy, planned ways—not through more impulse spending.

Final Thoughts

Stopping impulse spending isn’t about perfection—it’s about progress. By identifying triggers, delaying purchases, reducing convenience, setting boundaries, and focusing on meaningful financial goals, you can transform your spending habits permanently.

Small improvements today can lead to significant financial freedom tomorrow. Every time you resist an unnecessary purchase, you’re strengthening your financial discipline and moving closer to stability and peace of mind.

The goal isn’t to eliminate enjoyment—it’s to align your spending with what truly matters.

Start with one strategy today. Consistency will do the rest.